Kaspi Bank’s Digital Transformation Journey - from Almaty to the World: The Kazakh Super App

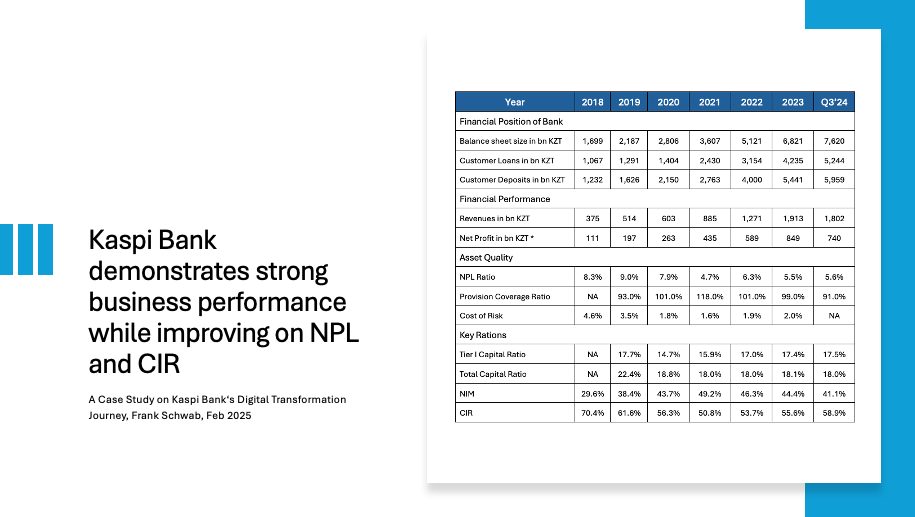

Kaspi Bank, headquartered in Almaty, Kazakhstan, has positioned itself as a leader in digital banking through its innovative Super App ecosystem. The bank integrates financial services, e-commerce, and payments, creating a comprehensive platform that caters to both consumers and merchants. This two-sided model includes the Kaspi.kz Super App for individuals and the Kaspi Pay Super App for businesses, transforming everyday financial and commercial transactions in Kazakhstan. Recognized as the "Best Digital Bank in Central Asia" by Global Finance in 2022, Kaspi Bank has achieved rapid financial growth, with its balance sheet expanding from USD 3.8 billion in 2018 to USD 16.8 billion by Q3 2024. Net profits have similarly soared, growing from USD 245 million in 2018 to USD 1.8 billion by 2023, reflecting a robust compound annual growth rate (CAGR) of 50%.

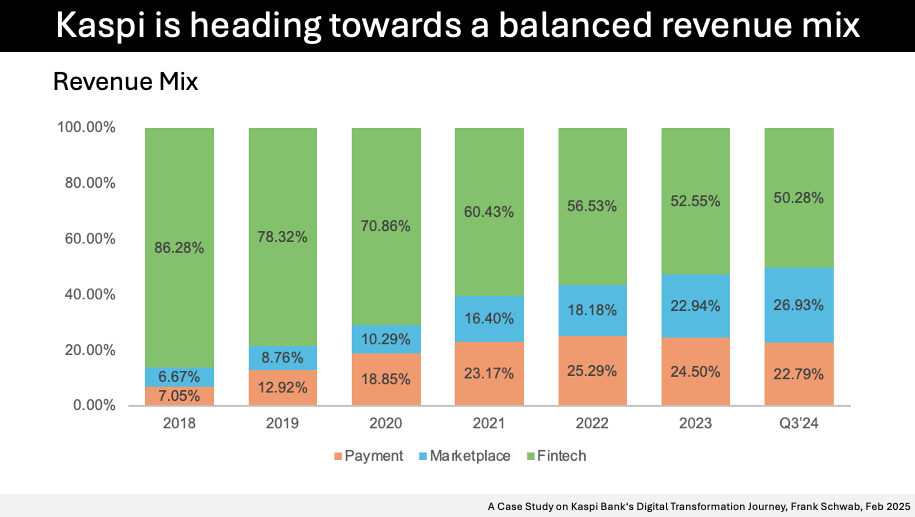

The bank's revenue model has evolved significantly, with its payments and marketplace segments now driving a substantial portion of its income alongside fintech services. Kaspi.kz has maintained a strong net interest margin (NIM), with the payments segment improving from 25% in 2018 to 65% in 2023. The bank's cost-to-income ratio (CIR) has declined from 70.4% in 2018 to 55.6% in 2023, showcasing operational efficiency through technological advancements and automation. Additionally, asset quality remains high, with the non-performing loan (NPL) ratio improving from 8.3% in 2018 to 5.5% in 2023, backed by a provision coverage ratio of 99%.

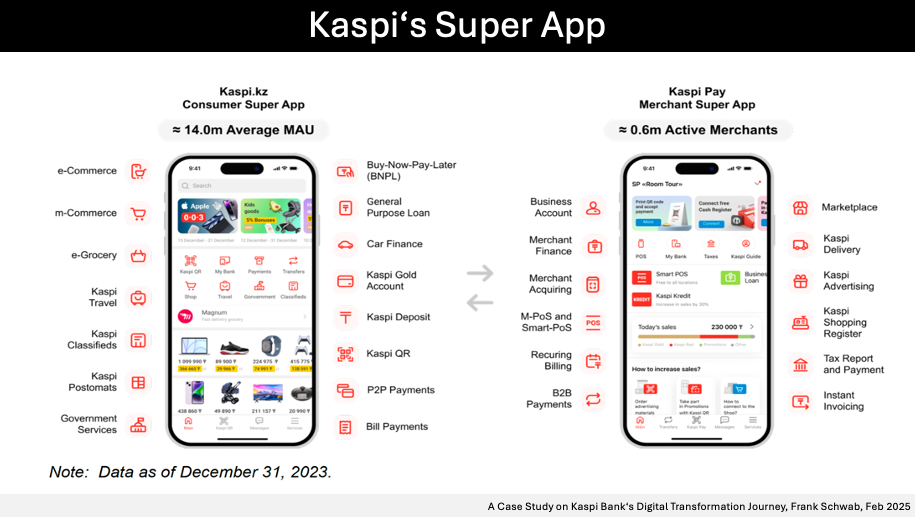

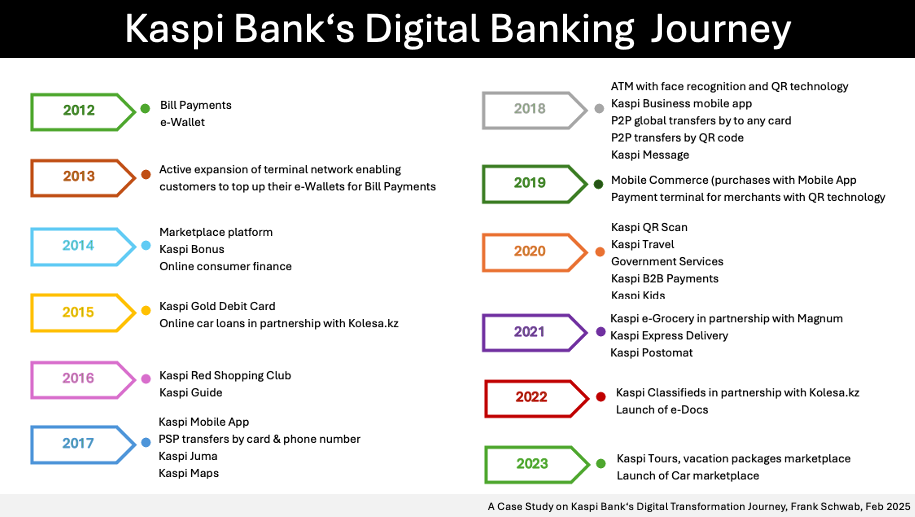

Kaspi Bank has expanded its digital ecosystem to include bill payments, peer-to-peer (P2P) transactions, mobile commerce, a shopping club, and a rewards program, making its Super App an integral part of consumers' daily lives. Its marketplace platform, Shop on Kaspi.kz, provides an extensive e-commerce experience, while Kaspi Pay facilitates digital transactions for businesses. The bank has successfully leveraged its extensive data analytics capabilities to drive product development, improve risk management, and enhance customer engagement. The introduction of artificial intelligence-driven financial tools and biometric-based security measures further streamlines operations.

Kaspi's fintech platform remains a key revenue driver, providing instant consumer loans, business financing, and buy-now-pay-later (BNPL) services. Deposits in Kaspi Bank have grown significantly, with an annual increase of 32%, reaching KZT 5,959 billion by Q3 2024. The bank has also extended its reach into government services, allowing users to access digital documents, register businesses, and handle tax payments through its Super App. Its logistics services, including Kaspi Delivery and Kaspi Postomats, enhance customer convenience and marketplace efficiency.

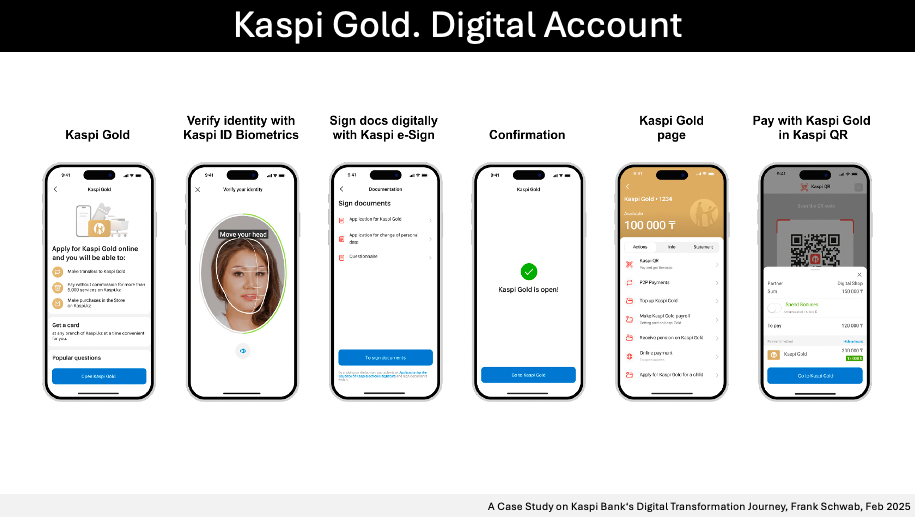

A crucial factor in Kaspi Bank's success is its deep integration of technology into all facets of its operations. The bank has invested in advanced data centers, AI-driven customer support, and automated self-service solutions, such as the Kaspi Kartomat, which issues debit cards in under a minute. This strategic focus on automation has contributed to an increase in productivity, with revenue per employee rising fivefold from 2018 to 2023. The bank has successfully reduced its reliance on physical branches, achieving higher operational efficiency while maintaining strong customer satisfaction.

Kaspi’s financial resilience is evident in its consistent revenue growth, with fintech, marketplace, and payments now contributing almost equally to the bank's net income. The payments segment, initially a smaller contributor, has grown to account for 37% of net income, while the marketplace and fintech segments contribute 31% and 32%, respectively. This balanced revenue mix ensures stability and long-term sustainability. The bank’s capital adequacy ratios have remained strong, providing a buffer against economic fluctuations.

Kazakhstan's economic environment has played a crucial role in Kaspi’s growth. The bank's balance sheet expansion significantly outpaced national GDP and banking sector growth rates. While Kazakhstan's GDP grew at an average rate of 4.1% between 2018 and 2023, Kaspi’s assets grew at a CAGR of over 30%, demonstrating its ability to capitalize on economic opportunities. The bank’s success in deposit mobilization, even during economic downturns, highlights strong customer trust and a well-executed liquidity management strategy.

Kaspi Bank's competitive strengths include its proprietary technology infrastructure, extensive data analytics capabilities, and a deeply embedded Super App ecosystem. With 14 million monthly active users and 732,000 active merchants by Q3 2024, the bank benefits from strong network effects that drive user engagement and business growth. Its strategic focus on customer satisfaction, as reflected in high net promoter scores (NPS), has enabled sustained market leadership. By continuously refining its offerings, Kaspi has built a business model that is both scalable and profitable.

Looking ahead, Kaspi Bank aims to expand its regional presence beyond Kazakhstan, leveraging its scalable Super App model. Recent acquisitions in Uzbekistan and Azerbaijan signal the company’s intent to penetrate new markets. The bank is also exploring opportunities in Central and Eastern Europe, aiming to serve over 100 million users in the coming years. Future growth initiatives include the expansion of B2B services, an enhanced advertising platform, and deeper integration into logistics and e-commerce.

Kaspi’s journey underscores the importance of a customer-centric approach, continuous innovation, and strategic ecosystem development. By prioritizing digitalization and seamless user experiences, the bank has not only revolutionized banking in Kazakhstan but has also set a global benchmark for digital financial services. Its success serves as a valuable blueprint for banks looking to embrace technology and redefine financial services in emerging markets.

✍️ Contact me to learn more about the in-depth case study and receive the comprehensive 46 pages report, featuring detailed analysis and multiple informative graphs.

http://www.FrankSchwab.de

#banking #strategy #digital #digtialtransformation #digitaljourney #casestudy

Published in CaseStudies, all on 25.02.2025 8:30 Uhr.