Why PEST is Still Relevant

PEST remains relevant as a strategic analysis tool for digital banks, provided it evolves to capture the nuances of the digital age. By focusing on how external factors specifically impact digital operations, PEST can help digital banks navigate the complexities of a rapidly transforming industry.

1️⃣ Political Factors

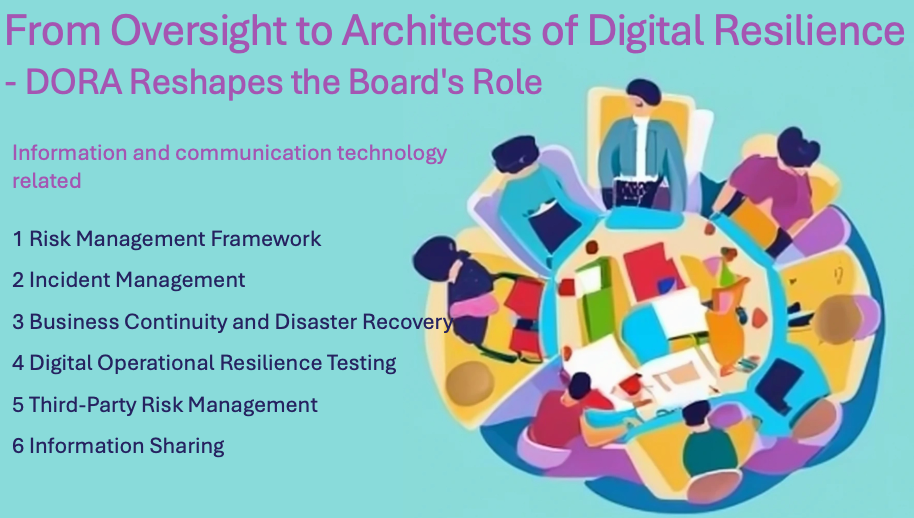

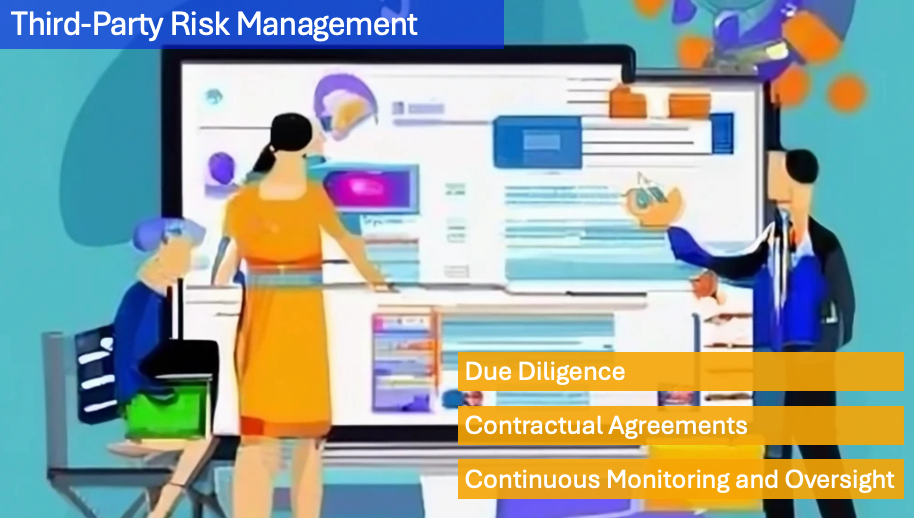

📌 Regulation & Compliance: AML, KYC, GDRP, DORA, …

📌 Licensing Requirements: which licenses are required?

📌 Government Initiatives: are there beneficial programs or restrictions?

📌 Cross-border Regulations: are there compliance requirements?

2️⃣ Economic Factors

📌 Interest Rate Environment: influence on profitability?

📌 Economic Downturns: appropriate risk management in place?

📌 Cost of Capital: funding secured?

📌 Consumer Spending and Saving Trends: impact on demand for digital financial products.

3️⃣ Social Factors

📌 Consumer Preferences: the growing demand for digital financial services.

📌 Trust & Security Concerns: how to deal with concerns about data privacy, fraud, and cyber security?

📌 Financial Inclusion: potential to reach underbanked or unbanked populations through mobile-first solutions.

📌 Demographic Trends: younger, tech-savvy consumers are more likely to adopt digital banking.

4️⃣ Technological Factors

📌 Innovation and Digital Transformation: rapid pace of technological innovation (AI, blockchain, cloud, …) is both an opportunity and a challenge.

📌 Cybersecurity Risks: a strong focus on cybersecurity and continuous investment in protecting customer data is essential.

📌 Fintech Integration: collaborations, partnerships, and APIs can expand service offerings.

📌 User Experience (UX) & Interface Design: intuitive, user-friendly, and accessible across various devices to retain and grow their customer base.

Published in strategy, banking, DigitalTransformation, all on 29.08.2024 9:30 Uhr. 0 comments • Comment here